IRS Audit Rates

The IRS reported audit rates continue to be low…very low. But that is now changing with thousands of auditors being hired for a post-pandemic scale-up of their reviews. So don’t get complacent. A closer look at the IRS data release reveals some audit pitfalls you should know about.

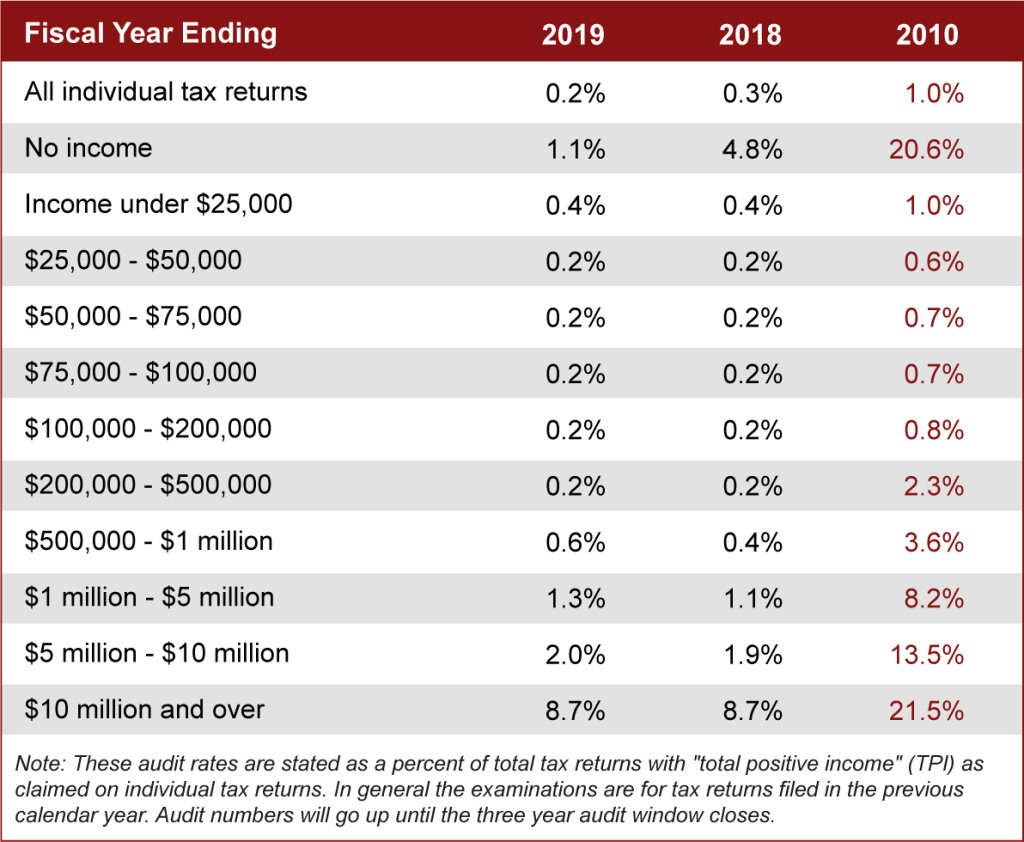

Audit Rate Statistics for Individuals

Source: IRS Data Books with 2019 audit figures updated through May 26, 2022

Observations

- Fewer audit examinations obscure the reality that you may still have to deal with issues caught by the IRS’s automated computer systems. While not as daunting as a full audit, you’ll need to keep your records handy to address any problems.

- Average rates are declining, but audit chances are still high on both ends of the income spectrum: no-income taxpayers and high-income taxpayers.

- No-income taxpayers are targets for audits because the IRS is cracking down on fraud in refundable credits designed to help those with low income, such as the Earned Income Tax Credit (EITC). And while not on the charts, 87% of Earned Income tax returns that are audited had additional tax applied!

- High-income taxpayers have long been a target for IRS audits. This group, however, saw a big decline in audit rates during the pandemic. Still, taxpayers with over $500,000 in income have more than double the chance of being audited than lower-income taxpayers. Not only do these taxpayers tend to have more complicated tax returns, but the vast majority of federal income tax revenue comes from them.

- Complicated returns are more likely to be audited. Returns with large charitable deductions, withdrawals from retirement accounts or education savings plans, and small business expenses (using Schedule C) are more likely to be the target of an IRS audit.

Stay Prepared

Always retain your tax records and supporting documents for as long as you need them to substantiate claims on a return. The IRS normally has a window of three years from the filing date to audit a return, but this can be extended if the agency believes there’s any fraudulent activity.

If you receive an audit letter from the IRS, it’s best to reach out for assistance as soon as possible.

Related Posts

-

Estimated Quarterly Tax Payments Guide for Schedule C Business Owners

If you’re self-employed, taxes don’t automatically come out of your income. That means it’s your responsibility to pay them throughout…

View More -

When Should You Switch From an LLC to an S-Corp for Tax Savings?

For many business owners, the S-Corp conversation starts with confusion and pressure. A friend mentions it. A Facebook group swears…

View More -

How The One Big Beautiful Bill Impacts You And Your Business

The One Big Beautiful Bill introduces tax changes that begin affecting returns filed in 2026. While the bill includes many…

View More -

Common Myths About Audits

Navigating an IRS audit can feel intimidating, but the truth is much simpler—and far less scary—than most people think. When…

View More